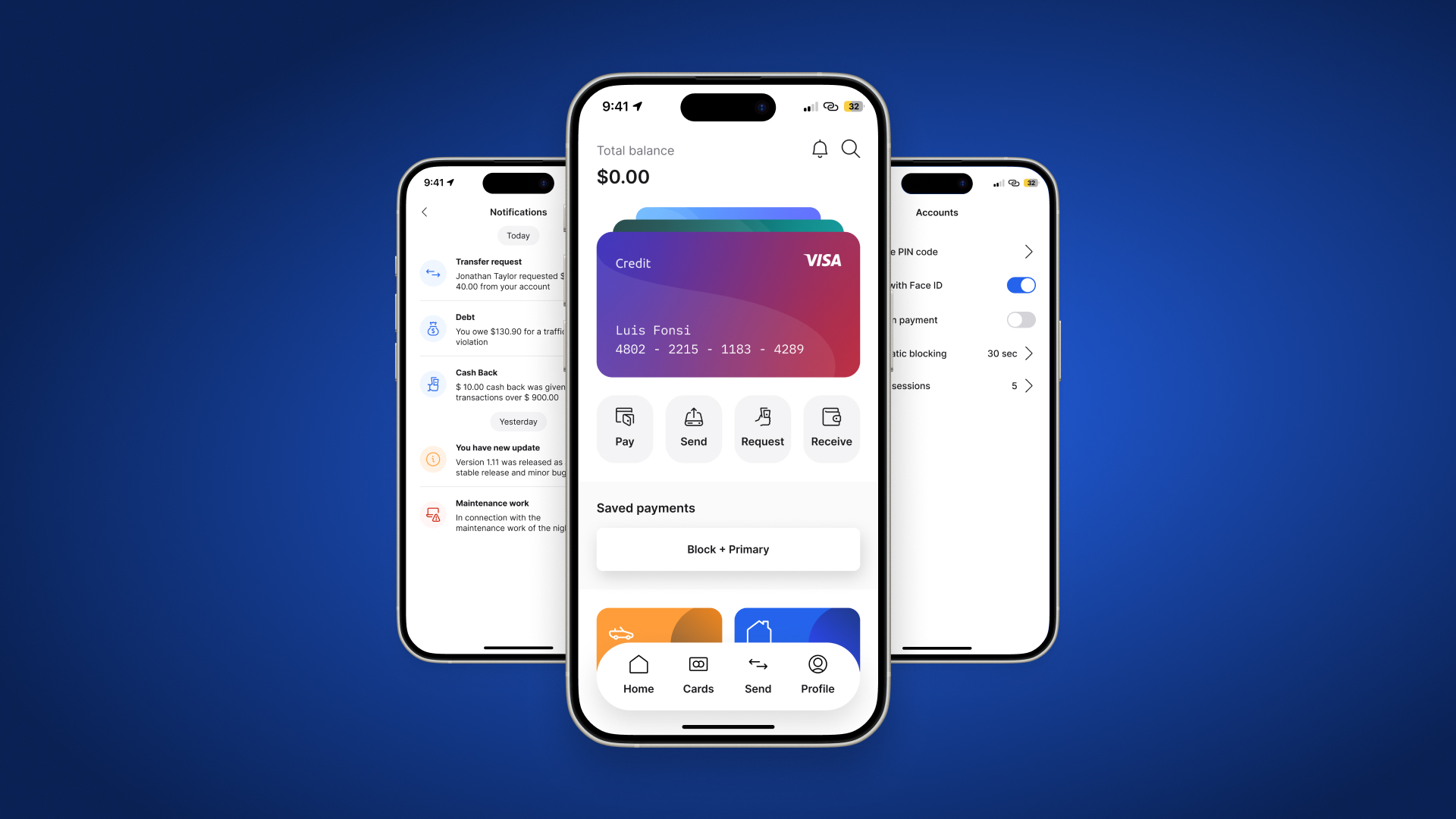

It is clear that the last couple of years brought some incredible new advances that drastically changed how we engage with our finances. Whether you need a new loan, a travel insurance or just some simple transaction processing, financial technology (or Fintech) companies are not only bringing a new digital revolution but also push traditional institutions to follow suit.

A recent survey by Market Screener shows that the Fintech market will be worth a whopping $26.5 trillion by 2022 and this growth is being fueled by many other sectors in need of easier access to investment options or loans so the future of Fintech seems almost limitless and right now even Amazon creating a bank doesn’t sound so unrealistic.

With such great potential, one might think that it is always just the sunny side of the road but in reality Fintech is currently facing some major obstacles and how key players in the field will handle these challenges will ultimately decide the next few years of fintech growth.

Lets see some of these and our main recommendations for tackling them:

- Compliance and Regulations

- Data Security and Privacy

- Growth Issues and Market Challenges

- Competition and Innovation

Regulations and compliance

Finance is one of the most regulated sectors and since the 2008 financial crisis, there is a dramatic increase in regulatory fees relative to earnings and credit losses. In addition to that, in the last few years new regulations like PSD2, which regulates payment services, and GDPR, which regulates data usage were also added to the picture. These regulations touch every aspect of the financial industry and as they are being rolled out, Fintech companies are constantly challenged to keep up and stay compliant not only to earn the necessary customer trust but also to get the equally important partners’ trust.

Although Fintech companies have a modern agile technology that is more advanced and usually free of the legacy issues that traditional financial institutions and their systems have, such big institutions have far more resources, processes, and documentation already set up, staff and expertise inhouse … Etc. that give them an upper hand that is hard to compete with. Non-compliance with AML (anti-money laundering) and KYC (know-your-customer) requirements can be extremely dangerous for any new Fintech startup because it can essentially stop them from gaining funds and establishing a customer base.

This might already seem enough but there is one more important aspect that limits international expansion and limits providing a unified offer globally. Attending the most recent FintechShow 5.0 we learned that even within the European Union there are significant differences in financial regulations. For example, the ever-so-popular BNPL (Buy Now Pay Later) solutions are not regulated uniformly so countries like Hungary consider BNPL as a type of traditional loan and as such have a much more strict set of rules than some other countries in the same region.

Another example is the digital banking license that many Neobanks use for their operation. After the UK left the EU, Lithuania became the No.1 European jurisdiction having the biggest number of issued Payment and Electronic Money Institutions licenses. The reason is that they provide much more favorable conditions enabling new companies to join the playing field easier and in some cases save millions of euros.

We can clearly see that as a result, even well-known players such as Revolut expand their market in small batches adding new countries in an almost one-by-one fashion.

Data Security and Privacy

Traditional banks have physical vaults, security guards, cameras, bulletproof doors, and many other clear measures to keep their assets safe but when it comes to virtual security, things start getting a lot more difficult to grasp. Vulnerabilities are much more discreet and potentially have more threats for users, as not only their money is at risk but their personal information is too, so it is clear why security is by far the biggest concern when it comes to mobile banking, payment solutions, and Fintech in general.

Of course, by now having two-factor authentication, biometric authentication, data encryption, and obfuscation, real-time alerting or even behavior analysis are all fairly standard measures but cybercrime is still on the rise, with new attacks occurring every 39 seconds. People rely on managing digital money increasingly more often, so Fintech companies now have more valuable data to protect than ever before which also makes them one of the hackers’ most common targets. Even large and reputable institutions, such as Pepperstone, a leading Australian brokerage, suffer from major data leaks as we could see when their customer data was stolen in August 2020.

It is obvious that a simple reactive approach to attacks is not enough and all Fintech companies should proactively improve day by day and try new methods to find possible vulnerabilities. Companies are using tools like cryptograms, which track the data they received to validate if it’s really coming from the given client or use AI fuzzing to find and abuse holes in their own code and ideally patch up these holes before cybercriminals discover them. However, hackers use the very same AI fuzzing and Machine Learning algorithms for their own goals which creates an endless race with the institutions they are trying to attack.

It is easy to see that this requires constant extra efforts, adds complexity and expenses, and requires security experts which sets the entry threshold for newly formed companies higher and higher.

Growth Issues and Market Challanges

This applies to most every startup in general but is especially true in a market where the majority of people still opt for traditional banking services. Finding and understanding a suitable niche, a clear target audience, and creating a strategy is the most essential step in not only acquiring new customers but also in the long term, for customer retention which proves to be equally important.

The competition was never this high with new Fintech companies popping up every single day so you not only need to have the best product fit but also a matching marketing and sales strategy to endorse your product by telling the right audience what you have created to help build brand awareness rapidly. We often find that startups excel at having an immense skill set in technology but their market strategy and customer acquisition plans lack far behind.

Our own internal experiences show that the pandemic greatly affected digital transformation and as such it equally affected online advertisements. Paid campaigns are all getting more and more expensive and certain (especially more broad) keywords skyrocketed in prices due to heavy competition so it is getting more and more important for new companies to know their niche very well from the get-go. Such industry standard and well-established advertising methods are squeezed out to the max but on the other hand new and maybe less established channels like TikTok, Snapchat or Reddit have less flexible options and give much more unpredictable results.

This means that the next generation of Fintech companies will not only need to be experts in financial technologies but also be advertisers really well versed in AdTech. Advertising technology, or AdTech, is a new term used to describe software tools and systems used to run and manage programmatic advertising campaigns. This often contains complicated processes that can be challenging to comprehend but in essence, it is based on using technology to buy and sell ad inventory through a data-driven process with the goal of helping publishers and advertisers optimize their ad campaigns and give the best results and ROI.

Competition and Innovation

Cloud computing, artificial intelligence, big data, blockchain, and machine learning are all the top buzzwords right now and it seems you can’t even start a new tech startup without having not only one but at least a combination of a few of them. At the same time, our recent survey shows that 58% of respondents are already fully satisfied with the financial solutions they use and couldn’t name a service or feature that they really miss from the current offerings. If we dive even deeper into the same survey results we see that most users are looking for easier access or more automated ways of handling the same old frequent tasks which (at least on the surface) make it seem that top-notch UX (user experience), seamless integration and clever automation is where current customer needs are mostly at.

New and innovative technologies combined with the lack of reputation can even make customers suspicious and reduce trust in the solution and even institutional or government partners can see it as a potential risk so there are forces in action that seemingly canceling out each other. Since de-risking has taken hold of the industry, Fintechs and money service businesses have faced distrust from banks which can be a massive barrier in getting a leg up in the market for countless Fintech companies.

In order to win the game, new Fintech startups need to have an effective partnership strategy that not only enables them to fit in the local financial ecosystem but also provides the support they can rely on when building their international growth. Some of the partnership highlights we see (even for traditional banks) are in paytech, identity protection and identity verification services and cryptocurrency investing.

Wrapping it up

There are indeed some significant challenges but as always most of them (with the right mindset) can become an opportunity that ambitious players can turn to their advantage and there are some fairly straightforward solutions that can go a long way.

We have internal Fintech Tuesdays here at Canecom where we tend to brainstorm about these ideas at great length so if you would like to be part of the discussion (at any day) please drop us a message.