“Open a bakery, they never go out of business” – my dad used to say.

As funny as it may sound, there are businesses like that where the general target audience of their service offered is 99% of the population so in theory, they are always needed. Quite similarly, everyone needs money to purchase goods so most everyone faces with financial technology on an almost daily basis. This is nothing new but the new situation that COVID-19 brought really shook things up and made certain fintech solutions skyrocket. Remote banking, cryptocurrencies or AI trading technologies are all on the rise, and the list only just started.

“According to the Global COVID-19 FinTech Market Rapid Assessment Study, the total number of digital transactions and new customers in the UK and Europe has increased by 17% and 21% respectively, year-on-year. It seems like there is a bright future ahead of fintech companies.” – Netguru

This is so true that the last few years made fintech one of key strategic focus areas for us here at Canecom. So, let’s see what are the latest trends we see in no particular order:

- Microservices for the masses

- Predictive Analytics

- Autonomous Finance

- Longevity Banks

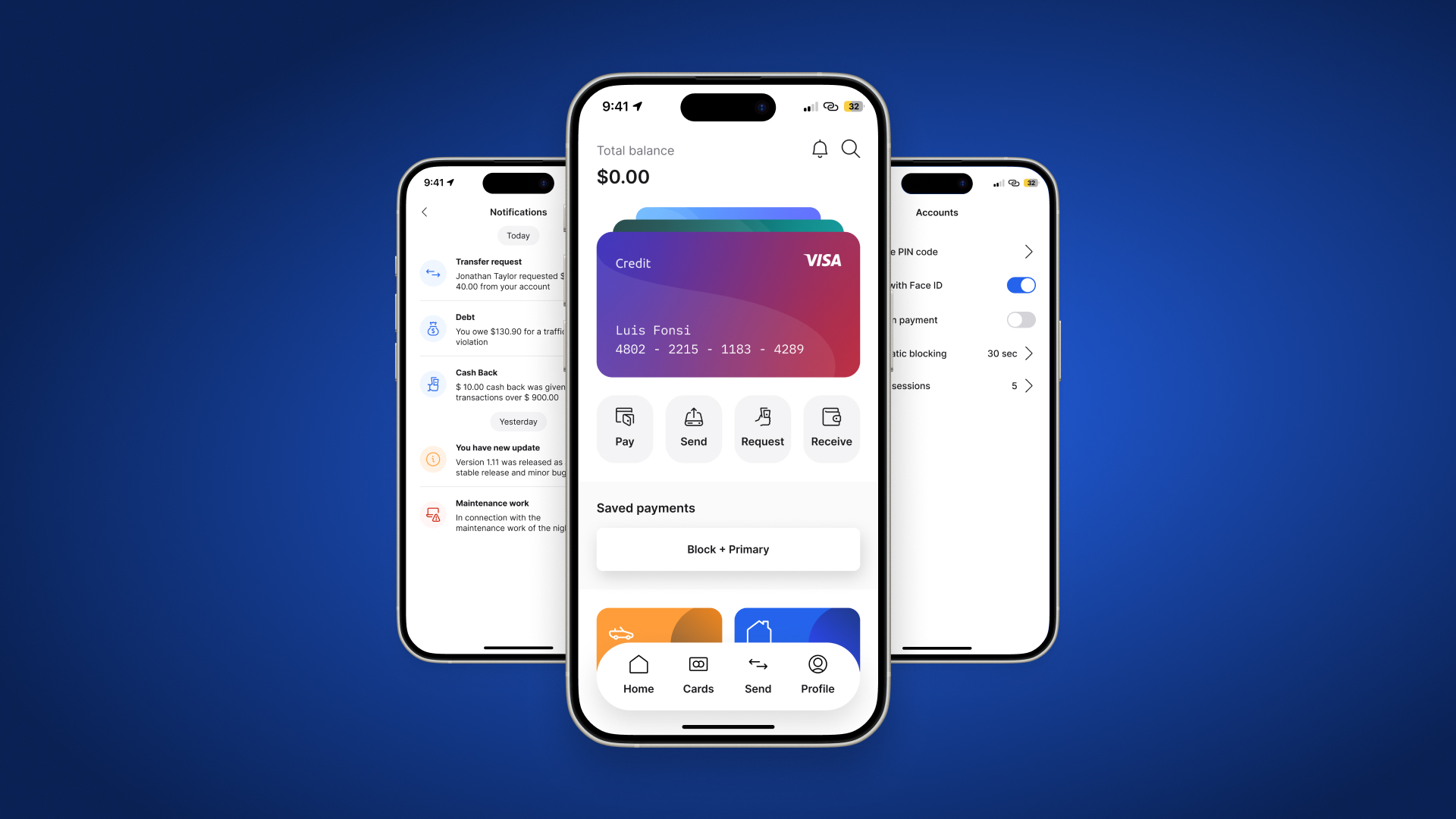

1. Microservices for the masses

Traditionally financial systems are not only hard to modify but also time-consuming and costly due to their monolithic nature but there was an extreme pressure on fintech providers to pace up to the new digital game.

Monolithic systems were built by using one code to create a single unit. The entire architecture had to be changed if a new need appeared as the platforms were highly interdependent. This created the strong need to come up with a new architecture that allows much better customization and also allows it with a much quicker turnaround.

Microservices have been introduced as a solution as they offer far greater flexibility, scalability and development speed. Microservices break the entire monolithic application into smaller, independent, deployable services around specific business capabilities. This not only made them the default approach for new start-ups but also made them become a favorite to re-architect existing applications. Even for large enterprises it became a must to update their tech stack to be able to keep up with the demand of the new era.

Businesses such as Amazon, PayPal, Capital One, and Monzo are showing their success with microservices. They have embraced microservice architecture to rapidly scale and deliver value to their customers with excellent results.

I would also highlight two recent sub-trends:

- Containers as they are one of the best ways to develop and deploy microservice-based applications. This is due to their capability of reducing overhead and efficiency. Kubernetes is one of the most popular choices as a container orchestration platform that brings applications from development to deployment rapidly. Containers have become one of the popular trends that is on rise for adoption.

- AI in microservices especially in the management of microservices. Whether load prediction, decay detection, security, personalization, or resource planning, the emergence of AI in microservices has made solving some of the major microservice management challenges a lot easier.

2. Predictive Analytics

As cyber-security continues to be one of the most difficult challenges that the financial industry faces, predictive analytics is playing a huge role in helping fraud protection and also strengthen all sorts of cybersecurity measures.

Machine learning, algorithms, and big data are all used for predictive analytics helping in assessing the likelihood of future events based on past customer behavior. The same technology can be used for improving customer experience and also for capacity modeling, both helping small and upcoming players to take on big corporations by providing a hyper-personalized and streamlined experience.

With modern Artificial Intelligence (AI) and Machine Learning companies can now create real-time data analytics that would have taken hours, days or even weeks 10 years ago. This real-time analytics allows data to be processed, measured, and evaluated immediately after entering a database creating the bases for predictive analytics.

- Fraud protection: we can now pick up on even the slightest differences in a user’s behavior. We are able to analyze discrepancies based on a user’s transaction history or, even some publicly available data such as social media.

This for example enables blocking transactions, large cash withdrawals, or access from unusual locations until it is confirmed by the customer.

- Modeling customer value: predictive analytics tools can automatically assess a customer’s credit history, transactions history, interactions with the government or even social media activity. As a result, financial providers can speculate any credit risks there may be and the net profit for different prospect customers giving them invaluable insights.

- Personalization: according to the McKinsey&Company Report, personalized experiences drive revenue growth up by 15% in the fintech industry. As the customers are any businesses most valuable assets the race for hyper personalization is on its way and it is driven by predictive analytic tools giving insights into social-demographic trends, spending habits, and many other factors.

3. Autonomous finance

In short, ‘autonomous finance’ or ‘autonomous banking’ is about trying to provide a stand-out user experience for customers by making it simpler to manage their money. With technologies like rule-based automation, artificial intelligence (AI) and machine learning (ML) we can identify patterns of behavior or ways of banking, and consequently customers can be given more of what they need access to in an easier and quicker way.

To give a simple example, if you see that a customer keeps repeatedly sending money to a certain account, you can start suggesting that maybe they should automate this. This enables fintech providers to create a feedback loop with the customer that allows making their financial decision-making much easier and stress-free over time.

“Just like you can put a destination in Google Maps and they’ll make the optimal route for you, Autonomous Finance allows you to put in your “financial destination” and the app will calibrate and calculate the path to get there.” – says QuHarrison Terry

4. Longevity Banks

As Margaretta Colangelo writes in Forbes: “The most capable client demographic in terms of purchasing power are the citizens of the 7th Continent which is made up of 1 billion people over 60. The global spending power of this demographic is expected to be $15 trillion this year. Who will serve this market? Longevity Banks and FinTech 2.0 services will attract people 60+ who want to optimize their wealth-span.”

Longevity Banks are going to rely on data and predictive models to determine who is likely to live a “longer than expected life” and suggest how to best serve the financial needs of such a group. Eventually, Margaretta even predicts that Longevity Banks could become retirement communities where they could perhaps pursue a longer life with longevity medicines and also build a structure that supports financial stability over time.

Even if the prophecy won’t be fulfilled, it is clear that age-friendly fintech companies will be on the rise as the human lifespan is on the rise which is great for both humanity and for compounding interest as well but this also means that people will either need to work longer or get better at saving if they want to enjoy a worry-free retirement.

Have a new fintech idea but you don’t know how to bring it to the market or you simply need a POC to validate the idea? Get in contact to discuss how we can help in setting the wheels in motion.